For the first time in more than 60 years, the Bureau of Land Management will force oil and gas companies to set aside more money to guarantee they plug old wells, preventing them from leaking oil, brine and toxic or climate-warming gasses.

The rule, finalized this month, comes at a critical time. Money previously set aside to clean up wells on federal land would have covered the cost of fewer than 1 out of 100, according to the government’s own estimates, and the vast majority of the country’s wells sit inactive or barely producing, meaning they’ll soon need to be plugged.

But the federal agency’s work falls short of protecting taxpayers from the oil industry’s cleanup costs, according to a ProPublica and Capital & Main review of contracts or other cost estimates at tens of thousands of wells across the country. While the updated rule will shrink the gap between companies’ financial guarantees to plug wells, known as bonds, and the cost of the work, it still leaves a significant shortfall.

One math error alone leaves taxpayers on the hook for roughly $400 million more than they should be. A Bureau of Land Management employee’s arithmetic mistake yielded an incorrect average cleanup cost for wells that the agency has plugged, largely at taxpayer expense. That artificially low cost estimate became the foundation of the new bonding requirements.

When ProPublica and Capital & Main pointed out the error in December, and that it could potentially cost taxpayers — and save oil companies — hundreds of millions of dollars when multiplied across the many thousands of wells the new rule would touch, the agency downplayed the miscalculation.

A spokesperson said the bureau “recognized the issues,” but they weren’t “significant enough” to correct. The proposed bond amounts are minimums, which “may be adjusted” through a review every five years. Staff can then demand companies set aside more money, the spokesperson said.

But over the most recent five-year period, oil companies ignored the Bureau of Land Management’s demands to increase their bonds more than 40% of the time, a ProPublica and Capital & Main review of agency data found. The final rule did not change how these reviews are carried out or enforced.

Evidence abounds of regulators’ past failures to hold the industry to account for cleanup: hundreds of thousands — potentially millions — of so-called orphan wells that companies have walked away from and left to the government to plug. Environmentalists, researchers and some politicians worry the window is closing to fix the problem while the industry is still profitable and there’s political momentum.

Interior Secretary Deb Haaland, along with environmental groups and taxpayer advocates, heralded the changes. “These reforms will help safeguard the health of our public lands and nearby communities for generations to come,” Haaland said. The Wilderness Society called the rule a “big step forward for the woefully outdated oil and gas program,” while the Sierra Club said it would help in “limiting harmful impacts to lands, wildlife and community health.”

Mark Squillace, a University of Colorado Law School professor who studies natural resources, agreed that the changes are an improvement over what was there before, “but it does not go far enough.” A ProPublica and Capital & Main investigation found that the country faces a shortfall well into the tens of billions of dollars between the cost to plug wells and the money available to do so. Unaddressed, those costs could be passed on to taxpayers.

“We have too many abandoned oil and gas wells that were not adequately bonded,” Squillace said.

Bad Math at the Bureau of Land ManagementThe Bureau of Land Management oversees an estimated 30% of the country’s mineral wealth, including oil and gas, but its oil bonding rules hadn’t been updated since they were written in 1951 and 1960, not even to account for inflation.

A 2019 Government Accountability Office report found that, as a result, bonds were insufficient to cover the cleanup costs of 99.5% of wells on federal land. (The bureau never fulfilled a public records request filed in May 2023 seeking updated details on bonds or a related request filed in September 2019.)

The Biden administration attempted to rectify bonding issues via the Inflation Reduction Act, but the Senate parliamentarian stripped reform provisions from the bill, saying they were not germane. The executive branch then launched a process to rewrite administrative rules that apply to the nearly 90,000 wells on federal public land, where cleanup costs vary widely depending on the depth and condition of the well, among other factors.

Republicans unsuccessfully attacked that process, with the House of Representatives in March passing a bill sponsored by Colorado Rep. Lauren Boebert to stop the rule and bar the agency from ever completing similar regulatory updates. It was not passed by the Senate.

The Bureau of Land Management published its final rule this month. It increased from $10,000 to $150,000 the minimum bond required to cover a group of wells, called a lease, and from $25,000 to $500,000 the minimum to cover all of a company’s wells in a state. The rule also requires the amounts to be adjusted every decade to account for inflation.

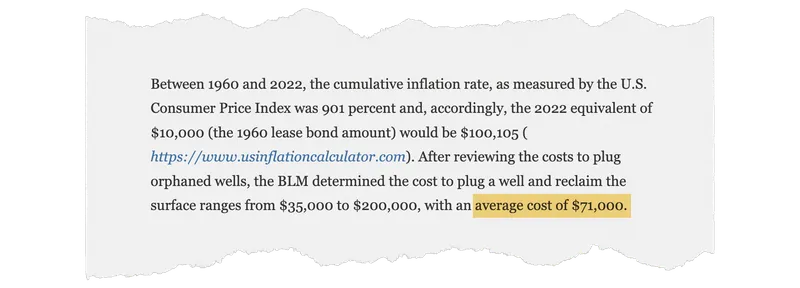

The agency based the required bond amounts on the cost to plug a typical orphan well, which it estimated to be $71,000. It drew from a narrow sample — 22 wells the agency recently paid to plug in three states — contending that was “a sufficient representation of wells to support the rulemaking.”

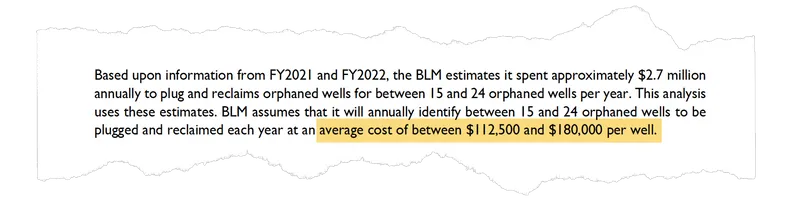

But the agency acknowledged higher per-well cleanup costs elsewhere in its own research, stating that it expects to spend between $112,500 and $180,000 to plug each orphan well in the future. The agency did not explain why it appears to contradict itself.

Adding to skepticism over the agency’s calculations, three wells included in the agency’s sample cost only $500 each to plug.

That figure is “hard to imagine,” said Chris McCullough, an engineer who previously managed complex plugging projects for California. At one site McCullough helped plug, two wells were leaking gas into a densely populated neighborhood a mile from Dodger Stadium. His crew spent $1.2 million overall to seal the wells, move infrastructure and set up a shuttle service for residents while the job was in progress.

Meanwhile, Bureau of Land Management records show that a single well in Alaska, for example, recently cost the government more than $13 million to plug. This project, however, was not included in the agency’s calculation. (An agency spokesperson said the well was “not a useful comparison” because plugging wells in Alaska includes costs that would be unusual at orphan wells in the Lower 48.)

The agency’s decision to factor in low-cost outliers while eschewing the most expensive sites ignores the reality that plugging wells brings unexpected challenges, according to geologist Dan Dudak, who also oversaw cleanup work for California and now owns an environmental consulting firm alongside McCullough. Doing such work in Alaska, Dudak explained, requires setting up “small, mobile, self-contained towns” to support “the personnel and equipment necessary to plug a single well.”

In the Lower 48, plugging costs are also high. Across Indian Country, for example, it would cost an average of more than $82,000 to plug a typical well, not counting the millions of additional dollars needed to first find the wells and study what sort of cleanup is needed, according to Interior Department data published in 2023. The department also allocated $150 million to plug roughly 600 polluting or dangerous orphan wells elsewhere on federal land — $250,000 per well.

Even more wells are plugged by states’ oil agencies, which recently offered a glimpse into what experts consider realistic plugging costs in their applications for federal funds to support that work. Alaska, California, New Mexico, North Dakota and West Virginia regulators all told the Interior Department that it takes more than $150,000 to plug a typical orphan well and address pollution around it.

Energy finance think tank Carbon Tracker Initiative in April published a report analyzing the impact the federal agency’s new bonding levels would have in Wyoming’s Big Horn Basin. The study, authored by petroleum reservoir engineer Dwayne Purvis, found that, while the rule would require drillers to set aside millions of dollars in additional bonds, it would still only be enough to cover 3% of the projected cleanup cost.

“Despite the progress in the new rules,” Purvis said after reviewing the final version, “I’m convinced that the situation merits much more financial assurance in one form or another than this change provides.”

While the Bureau of Land Management’s updated rule focused on how much money should be set aside to clean up wells, it ignored another looming threat: cracks in the key financial tool oil companies use as bonds.

In public comments on the rule, both environmental groups and oil industry representatives asked it to address the shriveling market for surety policies, which are the most common type of oil cleanup bond and are similar to insurance policies in that a third party guarantees wells are plugged.

The bureau did nothing to mitigate that risk in the final rule. As evidence that bonds are secure, the agency instead pointed to a Small Business Administration program that helps small oil companies obtain surety bonds if they aren’t financially strong enough to purchase such policies from the market.

Meanwhile, many insurers are already declining to provide surety bonds to oil and gas companies or are requiring unobtainable levels of collateral as drillers become a riskier bet, surety brokers in three oil-producing states and state regulators in several others confirmed to ProPublica and Capital & Main.

Trevor Gilstrap, senior vice president of AssuredPartners, an insurance brokerage firm, called the surety market “so stinking bad right now.” Surety providers, he said, went from asking oil companies for as little as no collateral when underwriting a bond a decade ago to between 50% and 100% collateral now.

“Throughout my more than a decade in the insurance industry, with a strong focus on placing insurance and bond programs for oil and gas companies, I have never encountered a more challenging surety market,” he wrote in a letter commenting on oil bonds in New Mexico.

Insurance providers’ shrinking interest is all the more reason to require sufficient bonds now before oil companies walk away from their wells, researchers and activists say.

“Challenges in the oil and gas surety market should be taken as a giant flashing alarm for the financial health of the oil and gas industry itself,” said Andrew Forkes-Gudmundson, who works on bonding reform with environmental group Earthworks. The government must take this moment seriously, he added, otherwise “they and the taxpayers will be left holding the bag.”

Do You Have a Tip for ProPublica? Help Us Do Journalism.

Got a story we should hear? Are you down to be a background source on a story about your community, your schools or your workplace? Get in touch.

ProPublica is a nonprofit newsroom that investigates abuses of power. Sign up for Dispatches, a newsletter that spotlights wrongdoing around the country, to receive our stories in your inbox every week.

ProPublica is a nonprofit newsroom that investigates abuses of power. Sign up for Dispatches, a newsletter that spotlights wrongdoing around the country, to receive our stories in your inbox every week.